Source: The content comes from "Tianfeng Securities", thank you.

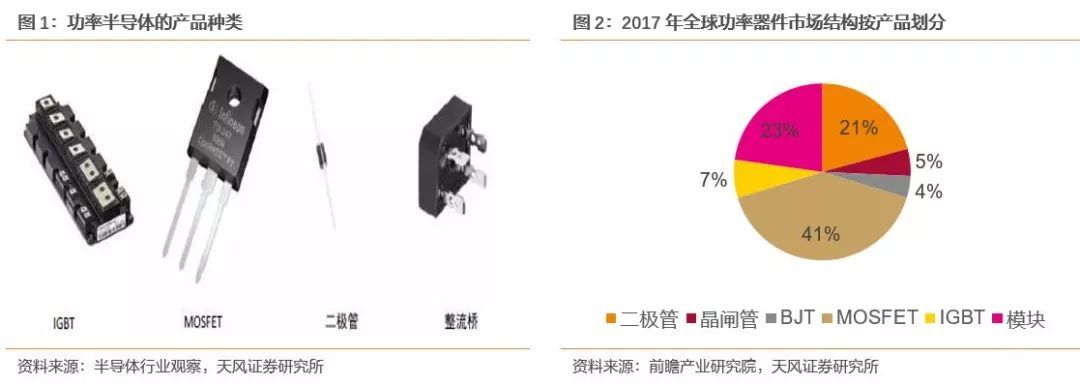

Power semiconductor devices are the core devices for implementing power conversion. The main uses include inverters and inverters. Power semiconductors can be classified into bipolar power semiconductors and unipolar power semiconductors depending on the type of carriers. Bipolar power semiconductors include power diodes, bipolar junction transistors (BJTs), power transistors (GTRs), thyristors, insulated gate bipolar transistors (IGBTs), and the like. Unipolar power semiconductors include power MOSFETs, Schottky barrier power diodes, and the like. Their operating voltage and operating frequency are also different. Power semiconductor devices are widely used in power electronics such as consumer electronics, new energy transportation, rail transit, power generation and distribution. Benefiting from the significant growth in demand for 5G and electric vehicles, we are optimistic about the market for power semiconductors.

1.2. Power semiconductor market structure

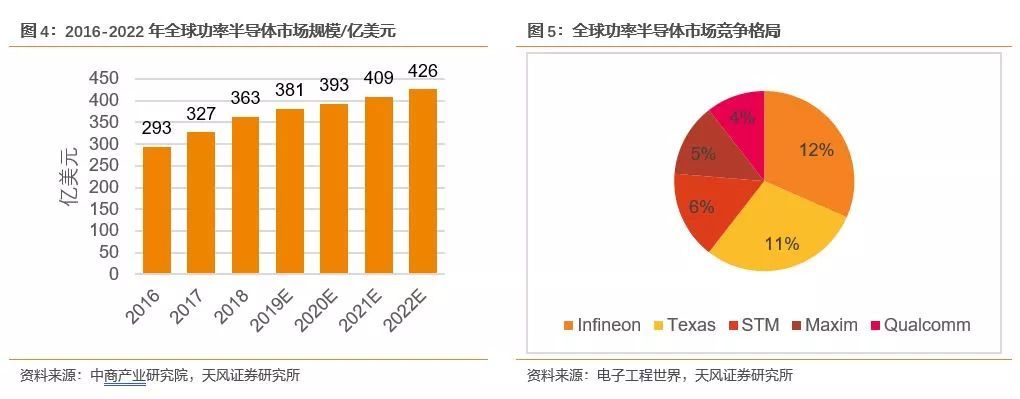

International manufacturers have a high level of manufacturing and have formed high professional barriers. We expect the global power semiconductor market to reach $42.6 billion in 2022. In the global power semiconductor market in 2015, Infineon ranked first with a market share of 12%. With their technology and brand advantages, Occidental and Japanese manufacturers account for 70% of the global power semiconductor device market. The mainland and Taiwan are mainly concentrated in the low-end power device market such as diodes and low-voltage MOSFETs. The high-end device market such as IGBT and medium-high voltage MOSFET is mainly occupied by European and American manufacturers.

We are optimistic about the domestic replacement space of power semiconductors. The research work on power semiconductors in China is relatively late, and it is restricted by capital, technology and talents. The power semiconductor industry as a whole shows the characteristics of a small number, a small enterprise scale, a low technical level and a scattered industrial layout. The original innovation problem has become an important factor hindering the development of the domestic power semiconductor industry. International power semiconductor manufacturers have not yet formed a monopoly of patents and standards. Compared with foreign manufacturers, domestic manufacturers have a competitive advantage in terms of serving customers and reducing costs. We believe that the domestic replacement space for power semiconductors is very broad.

1.2. Automotive Electronics Ignite Power Semiconductor Market

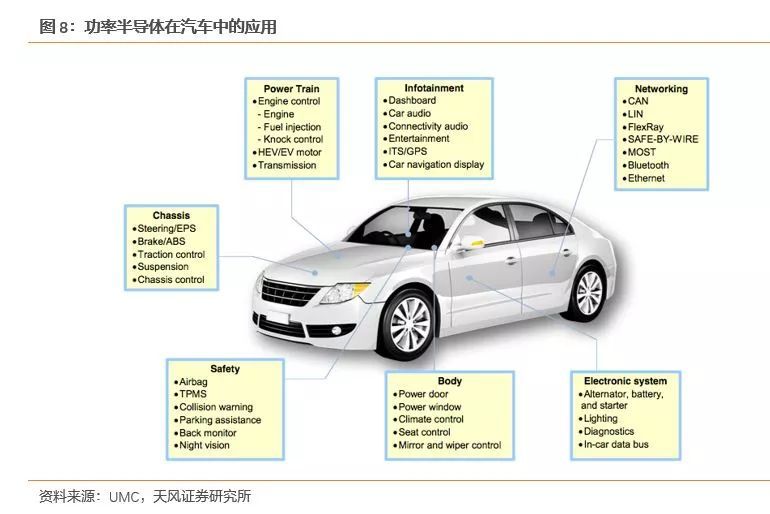

New energy vehicles have brought great growth potential to power semiconductors. A new energy vehicle is a vehicle that uses unconventional vehicle fuel as a power source, such as a pure electric vehicle or a plug-in hybrid vehicle. We expect China’s new energy vehicle sales to reach 2 million units in 2020, an increase of 53.8% year-on-year. New energy vehicles have added a large number of applications for power semiconductor devices. In 2020, the global automotive power semiconductor market will reach 7 billion US dollars. The three-phase asynchronous motor drive used in the Tesla model S model requires 28 IGBT chips for the drive control of each phase and 84 IGBT chips for the three phases.

China’s Ministry of Finance and the State Administration of Taxation jointly issued a notice: From January 1, 2018 to December 31, 2020, the purchase of new energy vehicles will be exempted from vehicle purchase tax and users will be encouraged to purchase new energy vehicles. We believe that the policy dividend will fully drive the market demand for power semiconductors.

2. IGBT - silicon based power semiconductor core

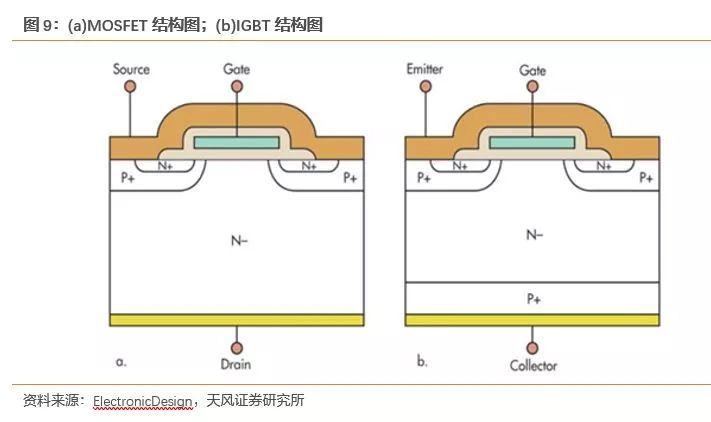

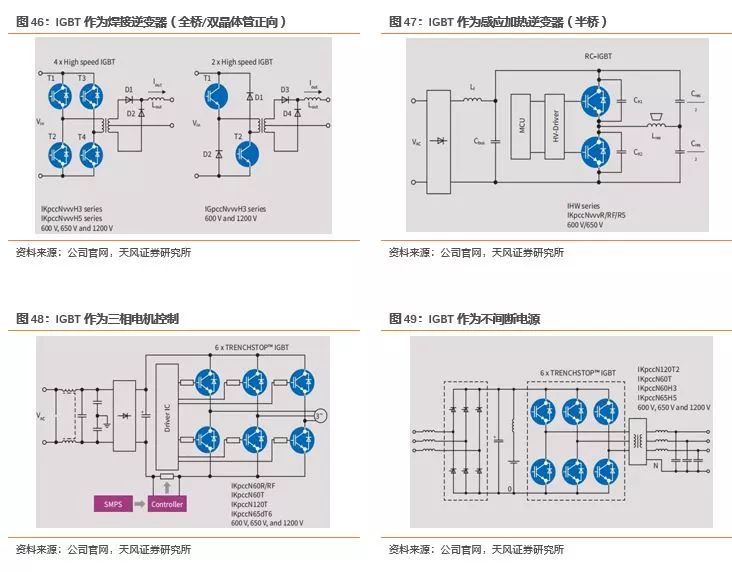

IGBT (Insulated Gate Bipolar Transistor), insulated gate bipolar transistor, is a composite full-controlled voltage-driven power semiconductor device composed of BJT (bipolar transistor) and MOS (insulated gate field effect transistor). The IGBT can realize the conversion between DC and AC or change the frequency of the current, and has the functions of inverter and frequency conversion.

In terms of structure, the IGBT has one more P+ region than the MOSFET, and the on-resistance of the device can be reduced by the injection of holes in the P layer. As the voltage increases, the on-resistance of the MOSFET also increases, so its conduction loss is relatively large, especially in high voltage applications. In comparison, the on-resistance of the IGBT is small.

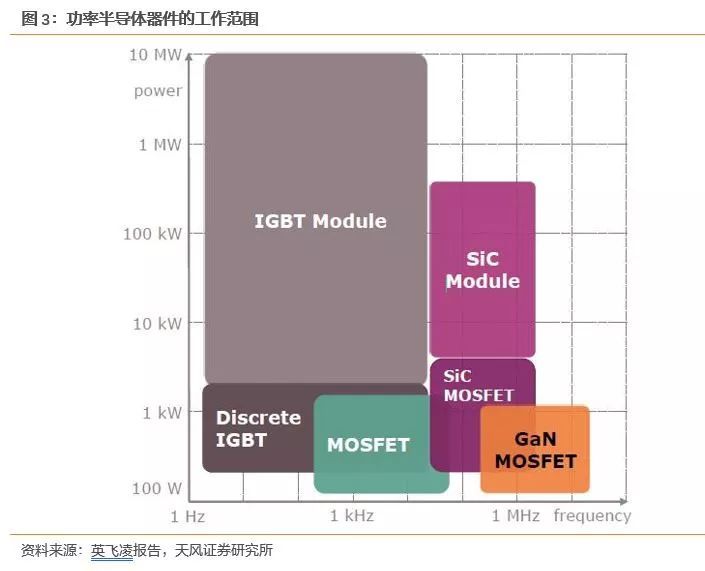

IGBTs are mostly used in the high voltage field, and MOSFETs are mainly used in the high frequency field. From the product point of view, IGBT is generally used in high voltage products, the voltage range is 600-6500V. The applied voltage of the MOSFET is relatively low, from a few ten volts to 1000V. However, the operating frequency of the IGBT is much lower than that of the MOSFET. The operating frequency of the MOSFET can reach more than 1MHz, even tens of MHz, while the operating frequency of the IGBT is only 100KHz. IGBTs are used in high voltage products such as inverters and inverters. The MOSFET is mainly used in high frequency products such as ballasts and high frequency induction heating.

2.1. IGBT market structure

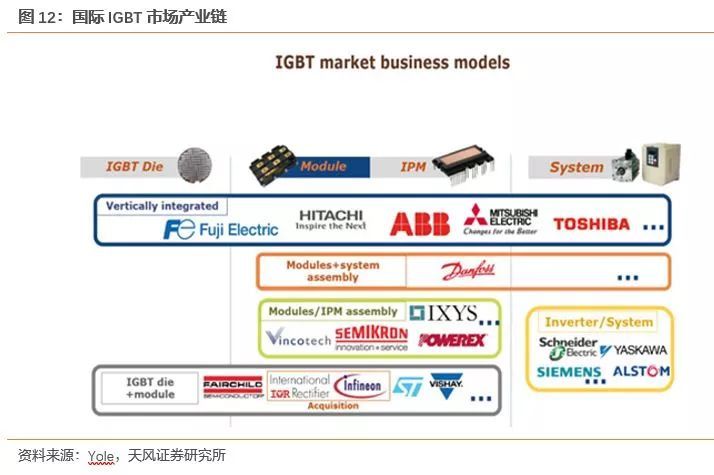

The main competitors in the global IGBT market include Infineon of Germany, Mitsubishi of Japan, Fuji Electric, American Anson, and Swiss ABB. The top five companies have a market share of over 70%. We expect the global IGBT market to reach US$6 billion in 2022, with huge incremental space. Foreign manufacturers have developed a complete range of IGBT products. Among them, Xiantong and other enterprises are in a dominant position in the consumer IGBT field. ABB, Infineon and Mitsubishi Electric have an advantage in the industrial grade IGBT field above 1700V. In the field of voltage levels above 3300V, Infineon, ABB and Mitsubishi Electric have a monopoly position, representing the highest level of international IGBT technology.

It still takes time for domestic catch-up. China’s power semiconductor market accounts for more than 50% of the world’s power semiconductor market, but 90% of mid- to high-end MOSFETs and IGBT devices rely on imports.

2.2. IGBTs are widely used, and new energy vehicles are important downstream growth engines.

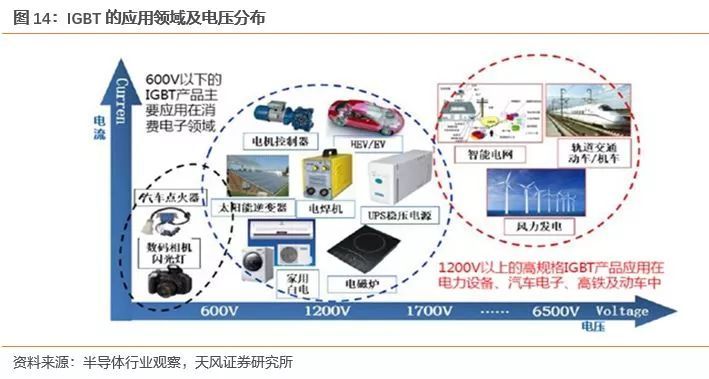

According to the voltage distribution, the IGBT products used in the consumer electronics field are mainly below 600V, such as digital camera flash. IGBTs above 1200V are mostly used in power equipment, automotive electronics, high-speed rail and motor trains. The IGBT modules commonly used in EMUs are 3300V and 6500V. The IGBT used in the smart grid is usually 3300V.

2.2.1. New energy vehicles

Motor control systems and charging posts are the main growth points for automotive IGBTs. Electric drive systems convert electrical energy into mechanical energy and drive electric vehicles. This is the most critical part of controlling electric vehicles. The IGBT belongs to the inverter module in the electric drive system, and the direct current of the power battery is inverted into an alternating current to be supplied to the drive motor. IGBT accounts for about 40% of the cost of new energy vehicle motor drive system and vehicle charging system, which is equivalent to 7-10% of the total cost of the vehicle. Its performance directly determines the energy utilization rate of the vehicle. The automotive semiconductor industry has a long certification cycle and very stringent standards. On the one hand, the mass consumption characteristics of the car make it more demanding on the life of the IGBT. On the other hand, the car is faced with more complicated working conditions, requiring frequent start and stop, climbing and wading, experiencing different road conditions and ambient temperature, etc., which is an extremely severe test for IGBT.

2.2.2. Rail transit

In the process of raising the speed from zero to 300 km in the short time of high-speed rail, IGBT is needed to ensure the accurate current and voltage required for traction converters and other electric equipment. IGBT has achieved comprehensive localization in the field of rail transit.

2.2.3. Smart Grid

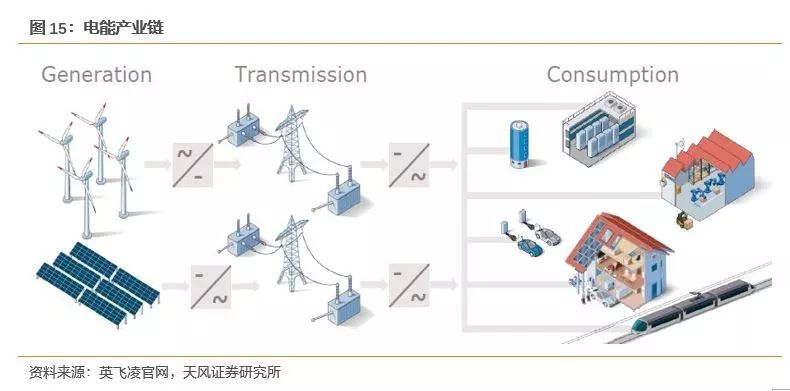

IGBTs are widely used in the power generation, transmission, power and power terminals of smart grids. From the perspective of power generation, IGBT modules are required for both wind turbines and rectifiers and inverters in photovoltaic power generation. From the perspective of the transmission end, the FACTS flexible transmission technology in UHV DC transmission requires a large amount of IGBT power devices. From the point of view of the transformer, IGBT is the key component of power electronic voltage transformation. From the point of view of power consumption, household LED lighting has a large demand for IGBT.

3. Third-generation compound semiconductors - broad prospects, industrial transformation

3.1. SiC - a break in the field of high voltage devices

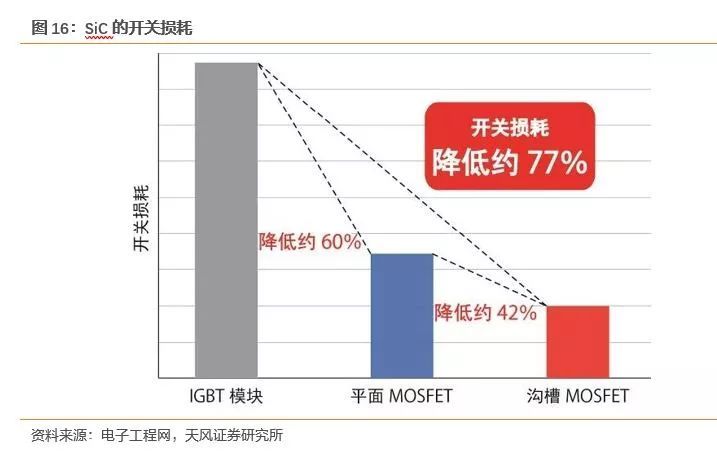

SiC is a representative of third-generation semiconductor materials. In terms of silicon, the current Si MOSFET applications are mostly below 1000V, which is between 600 and 900V. If it exceeds 1000V, the chip size will be large, and the switching loss and parasitic capacitance will also rise. SiC devices have advantages over Si devices in that they reduce energy loss, are easier to achieve miniaturization, and are more resistant to high temperatures. The loss of SiC power devices is about 50% of that of Si devices. SiC is mainly used to realize a small amount of lightening of a drive system such as an electric vehicle inverter.

Infineon and Career account for 70% of the global SiC market. ROHM is equipped with SiC power devices on Honda’s Clarity. Clarity is the world’s first fuel vehicle powered by Full SiC. Due to its high temperature operation and low loss, it can reduce the heat sink for cooling and expand the interior space. . Toyota’s fuel car MIRAI can seat four people, and Honda’s Clarity has a five-seater.

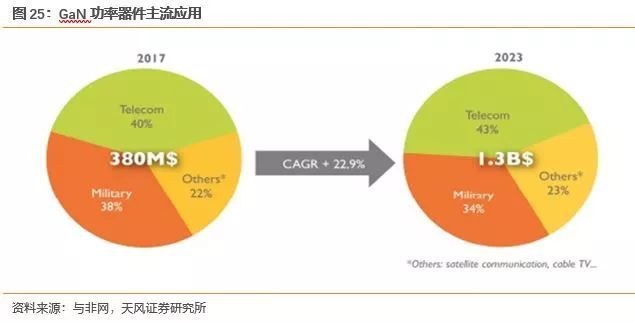

In 2017, the global SiC power semiconductor market totaled 399 million US dollars. It is estimated that by 2023, the total market will reach 1.644 billion US dollars, with a compound annual growth rate of 26.6%. From the application point of view, the growth rate of hybrid and pure electric vehicles is the highest, reaching 81.4%. In terms of products, SiC JFETs have the highest growth rate of 38.9%. Followed by the full SiC power module, the growth rate reached 31.7%.

The policy support has been greatly enhanced, pushing the third-generation semiconductor industry to overtake the curve. The state and local governments continue to introduce policies and industry support funds to support the development of third-generation semiconductors. In July 2018, China’s first "third-generation semiconductor power electronics technology roadmap" was officially released, and proposed the development path and industrial construction of China’s third-generation semiconductor power electronics technology. Fujian Province has invested 50 billion yuan to set up a special Anxin fund to build a third-generation semiconductor industry cluster.

3.2. GaN - Increased application scenarios, ushered in development opportunities

Due to the large band gap of GaN, GaN can be used to obtain semiconductor devices with larger bandwidth, larger amplifier gain, and smaller size. GaN devices can be divided into RF devices and power electronics. GaN’s RF devices include PA, MIMO and other base-to-base satellite and radar markets. Power electronic products include SBD, FET and other markets for wireless charging, power switching and other markets.

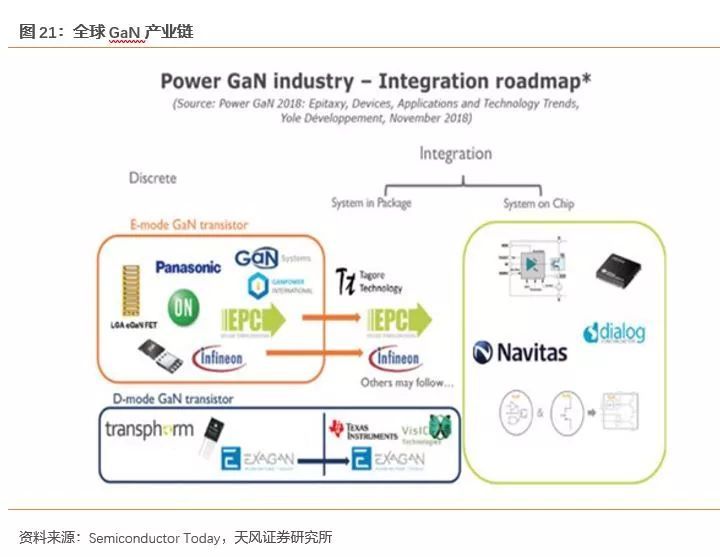

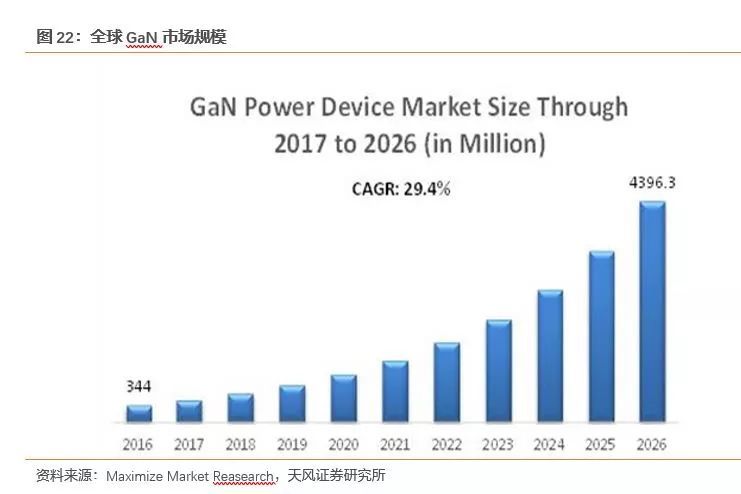

Infineon, ON Semiconductor and STMicroelectronics are the industry giants in the global GaN market. We expect the global GaN power device market to reach $440 million by 2026, with a compound annual growth rate of 29.4%. In recent years, more and more companies have joined the GaN industry chain. Such as start-up companies EPC, GaN System, Transphorm and so on. Most of them choose TSMC or X-FAB as their foundry partners. Industry giants such as Infineon, ON Semiconductor and STMicroelectronics use the IDM model.

3.3. SiC VS GaN - each has its own advantages, application drive

3.3.1. Basic characteristics

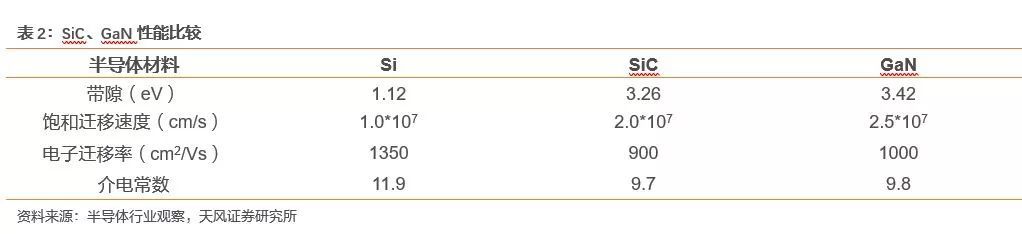

SiC is suitable for high voltage applications, and GaN is more suitable for low voltage and high frequency applications. A larger band gap allows the on-resistance of the device to decrease. The higher saturation migration speed enables both SiC and GaN to obtain faster, smaller power semiconductor devices. But an important difference between the two is thermal conductivity, which makes SiC dominant in high-power applications. GaN has a higher switching speed because of its higher electron mobility, and GaN has advantages in the high frequency field. SiC is suitable for high voltage applications above 1200V, while GaN is more suitable for high frequency applications of 40-1200V.

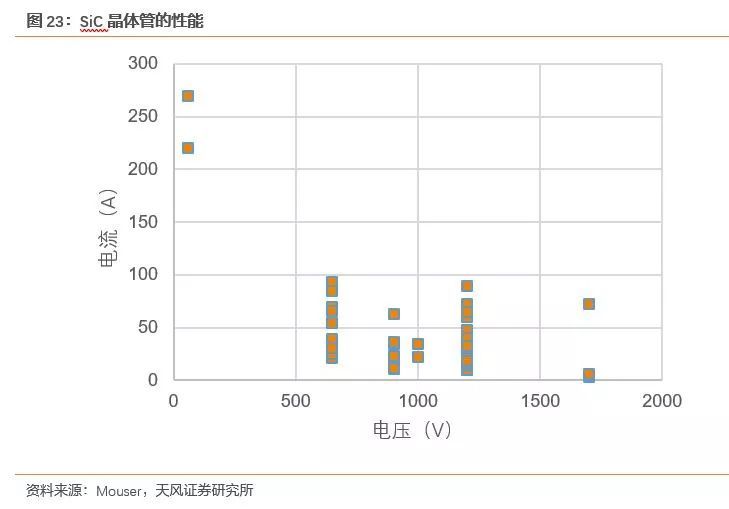

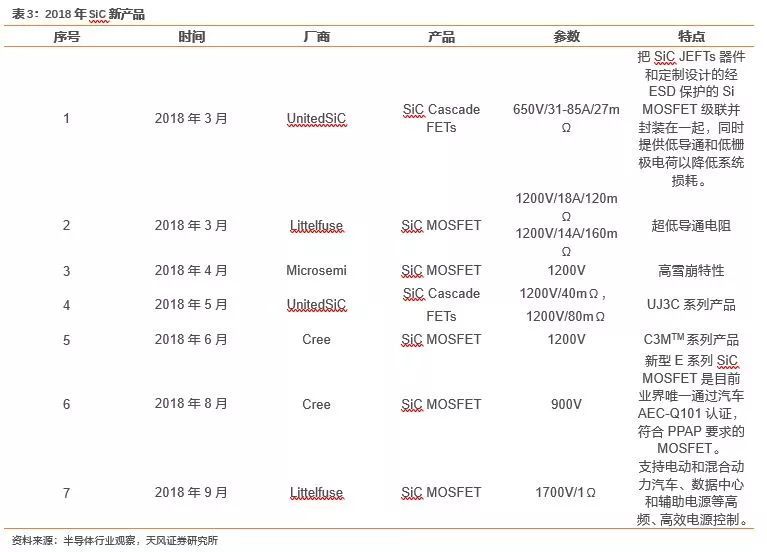

Commercially available SiC MOSFETs have a maximum operating voltage of 1700V, an operating temperature of 100-160 ° C, and a current of less than 65 A. The main products of SiC MOSFETs are 650V, 900V, 1200V and 1700V. Among the new SiC products introduced by major international manufacturers in 2018, Cree’s new E-series SiC MOSFETs are the only SiC MOSFETs in the industry that have passed the automotive AEC-Q101 certification and meet the PPAP requirements.

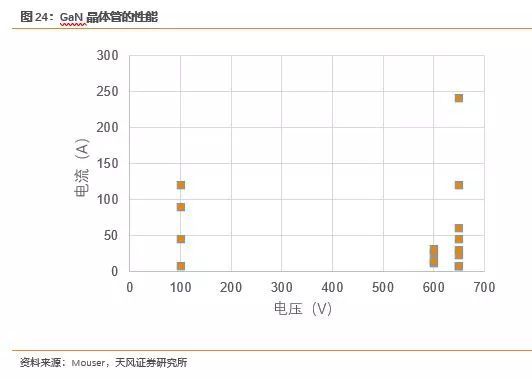

The current commercial GaN HEMT has a maximum operating voltage of 650V, an operating temperature of 25 ° C, and a current of 120 A or less. The main products of GaN HEMT are now 100V, 600V and 650V. Among the new GaN products introduced by major international manufacturers in 2018, GaN Systems’ GaN E-HEMT series achieves the highest current rating in the industry while increasing the system’s power density from 20kW to 500kW. The GaN HEMT produced by EPC is the first GaN product to receive automotive AEC-Q101 certification. It is much smaller than a conventional Si MOSFET and has a switching speed that is 10-100 times that of a Si MOSFET.

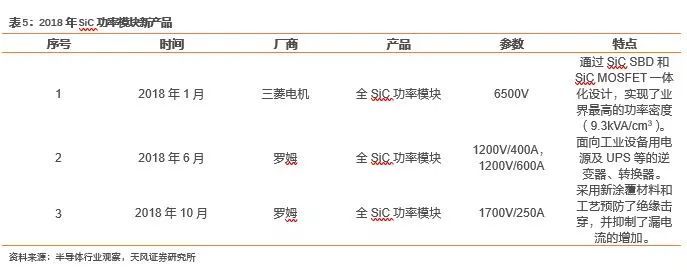

The current commercial SiC power module has a maximum operating voltage of 3300V. In January 2018, the all-SiC power module developed by Mitsubishi Electric was integrated with SiC MOSFET and SIC SBD to achieve the highest power density (9.3kVA/cm3) in the industry.

Commercial GaN power amplifiers currently operate at a maximum operating frequency of 31 GHz. In 2018, MACOM, Cree and other companies have successively launched GaN MMIC PA modular power products for base station, radar and other application markets.

3.3.2. Application scenarios

SiC is mainly used in photovoltaic inverter (PV), energy storage / battery charging, uninterruptible power supply (UPS), switching power supply (SMPS), industrial drives and medical markets. SiC can be used to achieve a small amount of lightening of a drive system such as an electric vehicle inverter.

Fast charging of mobile phones accounts for the largest share of the power GaN market. When GaN is applied to a charger, it can effectively reduce the size of the product. Currently, GaN chargers on the market support USB fast charging, with 27W, 30W and 45W powers. Leading smartphone maker Apple is also considering GaN technology as its wireless charging solution, which could lead to killer applications in the GaN power device market.

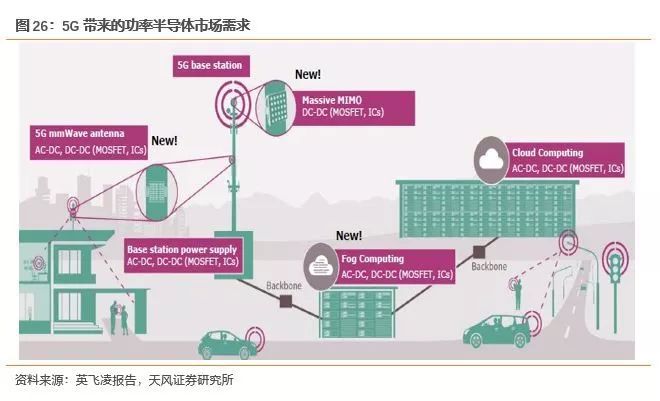

The 5G application is approaching and the RF GaN market is growing rapidly. The 5G main deployment frequency bands are sub-6-GHz for wide area coverage and 20 GHz or higher bands for high density areas such as airports. To meet the 5G requirements for higher data transfer rates and low latency, GaN technology is needed to achieve higher target frequencies. High output power, linearity, and power requirements also drive the conversion of PAs deployed by base stations from LDMOS to GaN. In addition, in the 5G key technology Massive MIMO, a large number of array antennas are used on the base transceiver station. This structure requires a corresponding RF transceiver unit, so the number of RF devices used will increase significantly. The use of GaN’s small size and high power density enables highly integrated product solutions such as modular RF front-end devices.

4. Power semiconductor market supply and demand and incremental space estimation driven by new energy vehicles

We derive the market demand for power semiconductors from new energy vehicles based on the value of bicycles in power semiconductors and the sales of new energy vehicles worldwide.

IGBT is the core component of the new energy vehicle motor control system. The three-phase asynchronous motor drive used in the Tesla Model S model requires 28 IGBT chips for each phase and 84 IGBT chips for the three phases. The price of each is about 4 to 5 dollars. We expect the IGBT’s bicycle value to be around $420. According to the global sales of new energy vehicles, the IGBT market demand brought by new energy vehicles can be derived.

SiC is mainly used to realize a small amount of lightening of drive systems such as inverters for new energy vehicles. In 2018, the Tesla Model 3 inverter used SiC MOSFETs manufactured by STMicroelectronics, each of which included 48 SiC MOSFETs. The Model 3 body is 20% smaller than the Model S. The price of each SiC MOSFET is about $50. We judge that the value of SiC’s bicycle is about $2,500.

The application of GaN technology in automobiles has just begun to develop. EPC’s GaN HEMT is the first GaN product to receive automotive AEC-Q101 certification. GaN technology can increase efficiency, reduce size and reduce system cost. These good properties make GaN automotive applications a hit.

We estimate the incremental space by measuring the supply and demand of IGBT/SiC new energy vehicles. Benefiting from the significant growth in demand for new energy vehicles, we believe that the incremental space for IGBTs is huge. There may be a shortage of supply in the SiC market. High cost is an important factor limiting the expansion of SiC capacity by international manufacturers.

5. Overseas & Domestic Power Semiconductor Important Companies

In 2017, the global market for power discrete devices and modules totaled $18.6 billion. Among them, Infineon ranked first with 18.6% market share. The second is ON Semiconductor and the third is STMicroelectronics.

In 2017, the global power discrete IGBT market totaled $1.1 billion. Among them, Infineon ranked first with 38.5% market share, and second with Fuji Electric. In 2017, the global power discrete MOSFET market totaled $6.65 billion. Among them, Infineon ranked first with a market share of 26.3%. The second is ON Semiconductor.

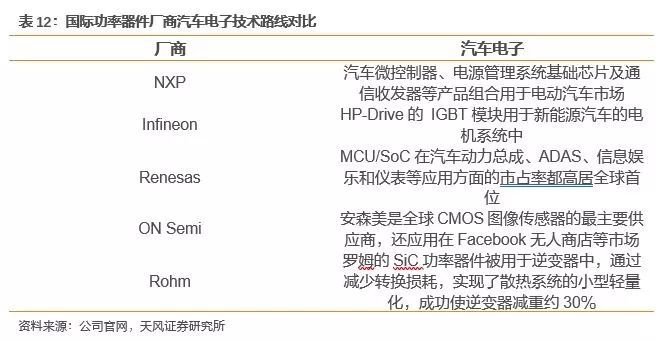

NXP’s revenues ranked first in the global power device market in 2017. Operating income was 6.548 billion yuan, net profit was 1.447 billion yuan, and net profit margin was 0.24. Infineon ranked second, with operating income of 5.526 billion yuan, net profit of 619 million yuan, and a net profit margin of 0.11.

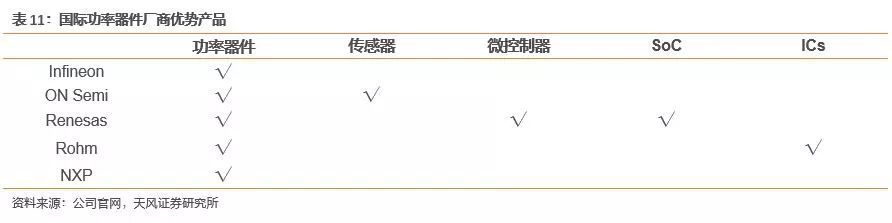

Each power device manufacturer has its own unique advantages. ON Semiconductor is the number one automotive image sensor company. In the global ADAS market, ON Semiconductor’s image sensors account for 70% of the market. Microcontrollers and SoCs are the main products of Renesas Electronics. Renesas Electronics is a leader in the global microcontroller market. Automotive electronics has become one of the important areas of competition for power device manufacturers.

5.1. Infineon

5.1.1. Introduction to Infineon

Founded in 1999, Infineon provides products and solutions worldwide in the automotive, power management and diversified markets, industrial power control and smart card and security businesses. Infineon is listed on the Frankfurt Stock Exchange (ticker symbol: IFX) and the US over-the-counter market OTCQX International Premier (ticker symbol: IFNNY).

According to Infineon’s 2017 financial report, the company’s fiscal year 2017 revenue of 5.526 billion yuan, an increase of 9.11%, net profit of 618 million yuan, an increase of 6.32%. The average net profit margin of the company in 15-17 is 10.13%, and the average ROE is 14.84%.

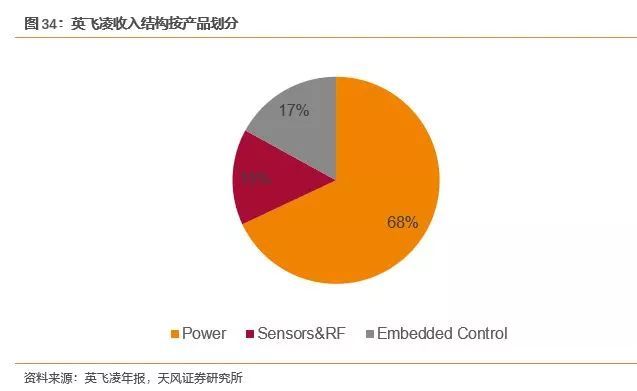

The company’s main products include power devices, sensors and RF devices, and embedded controllers. In the company’s revenue structure, power devices contributed the main income, with revenue of 3.757 billion yuan, accounting for 68%. Among the downstream customers of the company, customers in Europe contributed the main income, with revenue of 1.768 billion yuan, accounting for 32%.

5.1.2. Infineon’s technical advantages and product routes

Infineon introduces CoolSiC with Trench technology ? MOSFET series products. This design mitigates the conductivity of the planar channel and overcomes the problems between performance and robustness. In November 2018, Infineon took Sitectra’s cold cutting technology into the bag. Cold cutting is an efficient processing of crystalline materials that minimizes material loss.

HybridPACK? is a new line of power modules from Infineon designed for hybrid automotive applications. Automotive applications often require higher reliability, so Infineon has developed reverse-conducting IGBTs. In March 2018, Infineon and Shanghai Automotive announced the establishment of a joint venture to produce automotive-grade framed IGBT modules for the Chinese market.

IPC (Industrial Power Control) and PMM (Power management & Multimarket) are the core business units of Infineon. Among them, IPC’s main products are discrete and modular IGBTs. The discrete IGBT’s voltage operating range is 1200-1700V, and the module IGBT mainly works at 1200-6500V. PMM’s main products are: High Voltage MOSFET product series CoolMOSTM and medium and low voltage product series OptiMOSTM.

Infineon strengthens its core market with mature technology while opening up emerging markets with new technologies. Infineon strengthens the power semiconductor market through three strategies: 1) extending the SiC MOSFET and GaN MOSFET family and expanding its own unique 300mm wafer production. 2) Increase the investment in adjacent areas, such as the driver algorithm of the digital power control module. 3) Increase R&D in emerging markets, such as charging piles for electric vehicles.

Infineon’s CoolSiC ? The MOSFET portfolio will be extended in the coming years. The first step is to introduce different topologies, such as Sixpack and Halfbridge, covering power ranges from 2kW to 200kW.

Infineon’s CoolGaN ? The 400V electronic model is about to be developed. In 2015, Infineon and Panasonic reached an agreement to jointly launch an energy-efficient 600V GaN power device using Panasonic’s normally closed (enhanced) GaN transistor structure and Infineon’s surface-mount (SMD) packaged GaN devices. In June 2018, Infineon announced that it will begin mass production of CoolGaN 400V and 600V enhanced HEMTs by the end of 2018.

5.2. On Semiconductor

5.2.1. Introduction to Anson

Founded in 1999, ON Semiconductor focuses on key areas such as automotive functional electronics, vision and autonomous driving, body and comfort, in-vehicle networking and power management. ON Semiconductor is listed on the NASDAQ in the US under the ticker symbol ONNN.

According to the company’s 2017 financial report, the company’s revenue in 2017 was 3.623 billion yuan, a year-on-year increase of 41.88%. The net profit was 530 million yuan, a year-on-year increase of 345.19%. The average net profit margin of the company in 15-17 is 8.4%, and the average ROE is 19.41%.

The company’s main products include power and signal management, discrete and custom devices. ON Semiconductor is the world’s largest automotive image sensor company. In the global ADAS market, ON Semiconductor’s image sensors account for 70% of the market.

5.2.2. Advantages and product routes of ON Semiconductor

ON Semiconductor’s SiC technology features a unique patented termination structure that provides higher avalanche energy, the industry’s highest non-clamping inductive switch (UIS) capability and lowest leakage current. ON Semiconductor is about to introduce 1200V SiC MOSFETs and 650V GaN MOSFETs. ON Semiconductor’s MOSFET products are mainly concentrated in low to medium voltage.

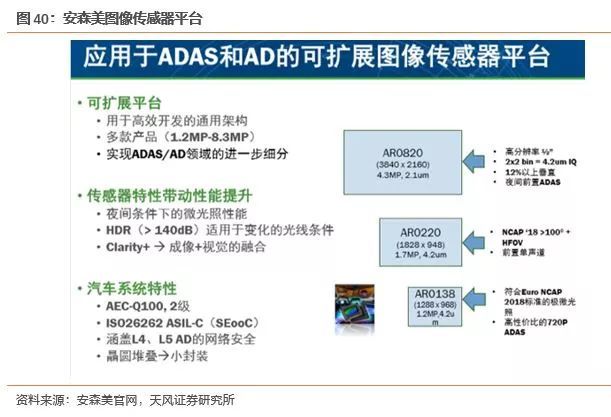

ON Semiconductor focuses on the convergence of the automotive sensor market. ON Semiconductor is the first company to offer professional image sensors for the automotive market. With its low illumination resolution and wide dynamic range, ON Semiconductor’s products can directly meet the needs of the A5 driving range. In 2017, ON Semiconductor acquired the IBM Radar Design Center. In addition to image sensors, it now offers a more complete sensor fusion solution including Radar and Lidar.

5.3. ROHM

5.3.1. Introduction to Roma

Founded in 1958, ROHM is one of the world’s best known semiconductor manufacturers and is headquartered in Kyoto, Japan. In 1983, Roma was listed on the Osaka Stock Exchange under the stock code 6393.

According to the company’s 2018 financial report, the company’s fiscal year 2018 revenue was 2.345 billion yuan, an increase of 12.81%, net profit of 220 million yuan, an increase of 40.92%. The average net profit margin of the company in 15-18 years was 8.06%, and the average ROE was 4.09%.

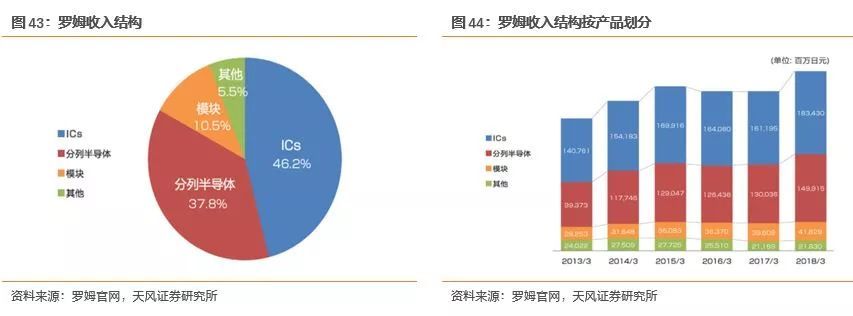

The company’s main products include ICs, discrete semiconductors and modules. In the company’s revenue structure, ICs contributed major revenues, with revenue of 183 million yen, accounting for 46.2%. Followed by discrete semiconductors, revenue of 150 million yen, accounting for 37.8%.

5.3.2. ROHM technical advantages and product routes

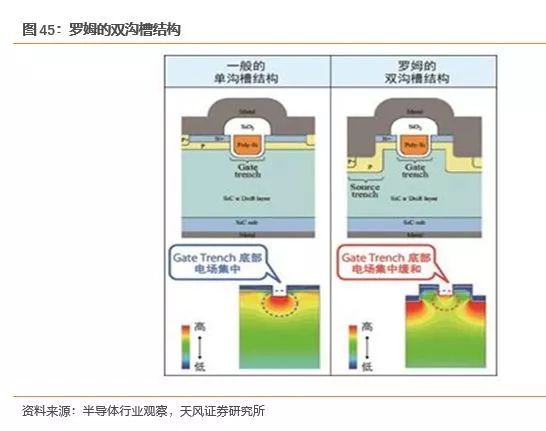

The dual trench SiC MOSFET is a representative product of ROHM. To further reduce power consumption, ROHM became the world’s first company to develop a dual-trench SiC MOSFET and mass production. With its unique double-groove structure, ROHM increases the strength of the door level and enables energy savings in electric vehicle electric drive systems such as inverters. Compared to IGBTs, the conversion loss of ROHM’s new generation SiC MOSFETs is reduced by 73%. In addition, ROHM has developed the 650V voltage-resistant IGBT "RGTV series (short-circuit withstand capability)" and "RGW series (high-speed switching version)", which combine the industry’s top low conduction loss and high switching characteristics.

ROHM focuses on the automotive and industrial markets. Consumer electronics is Roma’s largest application market, accounting for 57% of total revenue. Therefore, Roma hopes to increase investment in other fields such as automobiles. ROHM’s focus in the automotive sector is on powertrain, body, and analog power products from ADAS. In the industrial sector, the focus is on plant automation, energy and infrastructure.

5.4. Wentai Technology

Wentai Technology, established in 1993, was listed on the Shanghai Stock Exchange in August 1996 with a stock code of 600745. The company’s main business is the development and manufacture of mobile terminals, intelligent hardware and other products. Wentai’s main products include smartphones, laptops, and other hardware.

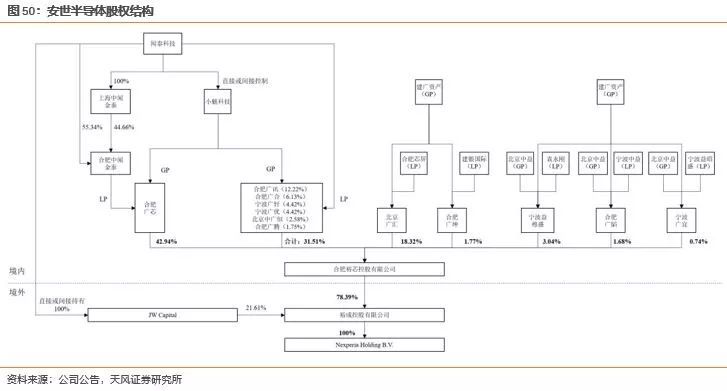

Acquisition of Anshi Semiconductor’s layout of the automotive sector. Anshi Semiconductor was formerly the standard product division of NXP and was acquired by domestic capital in 2017. This is also the largest overseas acquisition in the history of China’s semiconductor industry. In the automotive field, Anshi’s terminal manufacturers include international first-line brands such as BMW and Maserati. The acquisition will expand Anshi’s share of the consumer electronics market.

According to the company’s 2017 financial report, the company’s fiscal year 2017 revenue of 16.916 billion yuan, an increase of 26.08%, net profit of 335 million yuan, an increase of 74.48%. In 2017, the company’s gross profit margin was 8.98%, and the net profit margin was 1.98%.

Anshi Semiconductor’s medium and low voltage MOSFETs are leading the world. The main products of Anshi Semiconductor include discrete devices, logic devices and MOSFET devices. In the automotive field, Anshi’s main customers include Bosch, BYD, etc.; in the field of mobile and wearable devices, there are Apple, Google, Samsung, Huawei, Xiaomi, etc.; in the consumer field, there are Dajiang, Dyson, LG and so on.

5.5. Taiwan shares

Taiwan-based shares were established in 2004 and listed on the Shenzhen Stock Exchange in January 2010 with a stock code of 300046. The company specializes in the research and development of high-power thyristors and modules, and is a leading supplier of high-power semiconductor devices in China.

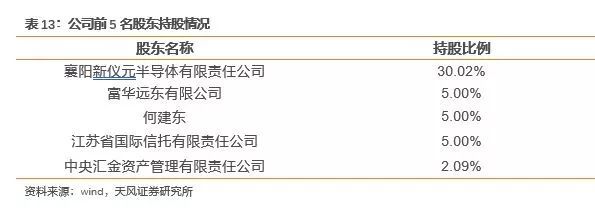

Among the company’s shareholding structure, the largest shareholder is Xiangyang Xinyiyuan Semiconductor Co., Ltd., with a shareholding ratio of 30.02%.

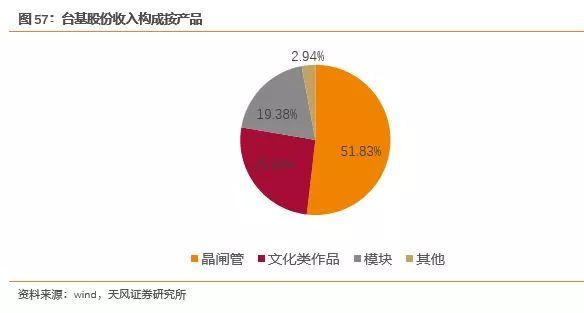

According to the company’s 2017 financial report, the company’s fiscal year 2017 revenue of 279 million yuan, an increase of 15.10%, net profit of 55 million yuan, an increase of 35.90%. In the company’s income structure, thyristors contributed the main income, accounting for 51.83%. Followed by cultural works, accounting for 25.84%.

With the rise of the new energy vehicle market, the company is expected to benefit in depth. The main products of Taiwan-based shares include high-power thyristors, high-power semiconductor modules, and power semiconductor components. At present, the company has formed an annual capacity of 2.8 million high-power thyristors. The company will focus on the development of new IGBT modules and intelligent devices such as IGCT, while tracking the third generation of wide bandgap semiconductor devices represented by SiC and GaN.

The funds raised are intended to be used in new high-power semiconductor device industry upgrade projects. In order to enhance the company’s profitability and core competitiveness, the company is planning non-public offerings. Among them, the project includes the construction of a sealed test line with a monthly output of 40,000 IGBT modules (compatible with MOSFETs, etc.), which is compatible with the packaging and testing of 150,000 SiC and other wide-bandgap semiconductor power devices. In addition, the company plans to invest 100 million yuan to invest in Beijing Yizhuang Economic Development Zone to set up a wholly-owned subsidiary Beijing Taiji Semiconductor Co., Ltd. to optimize the company’s product structure and business scope, and create new business growth points.

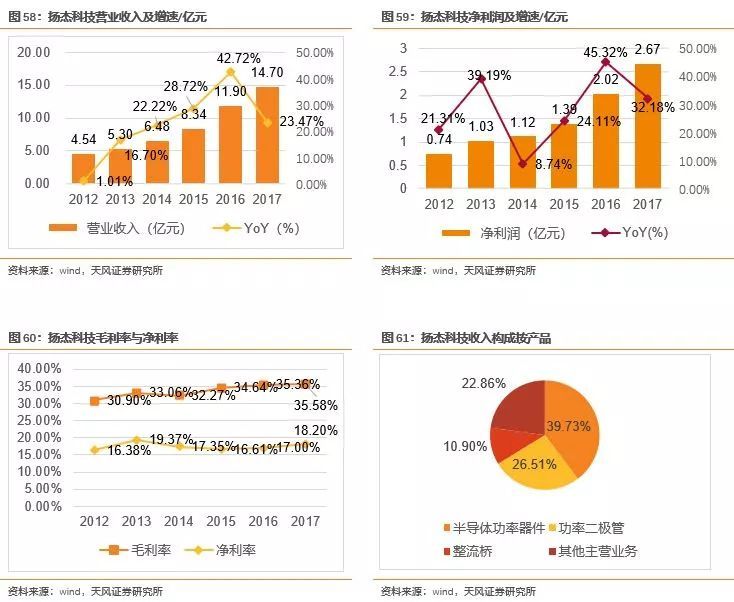

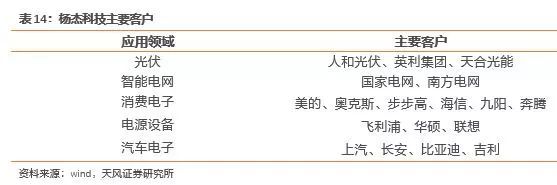

5.6. Yangjie Technology

Yangjie Technology, established in 2006, was listed on the Shenzhen Stock Exchange in January 2014 with a stock code of 300373. The company’s main business is the development, manufacture and sale of electronic components such as power diodes and rectifier bridges. Currently, Yangjie has 3, 4, 5, and 6-inch fabs, and 8-inch fabs are under planning.

According to the company’s 2017 financial report, the company’s fiscal year 2017 revenue of 1.47 billion yuan, an increase of 23.47%, net profit of 267 million yuan, an increase of 32.18%. Yang Jie controls costs through the IDM model, and the profit indicators lead the market. In 2017, the company’s gross profit margin reached 35.58%, and the net profit margin was 18.20%. Among the company’s revenue structure, power semiconductor devices contributed the main income, accounting for 39.73%.

Expand downstream application business and improve core competitiveness. The main products of Yangjie Technology include semiconductor power devices, power diodes, rectifier bridges and so on. The company is based on the fields of consumer electronics, security and photovoltaics, and vigorously expands the high-end market of automotive electronics and industrial frequency conversion.

5.7. Silan Micro

Silan Micro, established in 1997, was listed on the Shanghai Stock Exchange in March 2003 with a stock code of 600460. The company is mainly engaged in the design, manufacture and sale of electronic components. The company relies on the IDM model to improve product quality, strengthen control costs, and provide differentiated products and services to customers, greatly improving product penetration.

According to the company’s 2018 financial report, the company’s 2018 fiscal year revenue of 3.026 billion yuan, an increase of 10.36%, net profit of 74 million yuan, an increase of -28.16%. The average gross profit margin of the company in 16-18 is 22.28%, and the average net interest rate is 3.35%.

The featured process platform supports the development of semiconductor power devices. In terms of process platform, the company has completed the ultra-thin trench gate IGBT, super-junction high-voltage MOSFET, high-density trench gate MOSFET, etc. based on the stable 5- and 6-inch chip production lines and the 8-inch chip production line that has been successfully put into production. Development of power devices.

Continue to expand production capacity, the company entered a rapid growth period. In December 2017, Silan Micro signed a strategic cooperation agreement with the Haishu government of Xiamen. According to the agreement, the project has a total investment of 22 billion yuan, aiming to build two 12-inch specialty process wafer production lines and an advanced compound semiconductor device production line in Haishu District.

*Disclaimer: This article was originally created by the author. The content of the article is the author’s personal point of view. The semiconductor industry observation reprint is only to convey a different point of view. It does not mean that the semiconductor industry observes the endorsement or support of this view. If there is any objection, please contact the semiconductor industry for observation. |

Sale.

Sale.